Investors should carefully consider the objectives, risks, charges and expenses of the Fund before investing. This information and other information about the Fund can be found in the prospectus and summary prospectus. For a prospectus or summary prospectus please visit our website at https://usmutualfund.bailliegifford.com. Please carefully read the Fund’s prospectus and related documents before investing. Securities are offered through Baillie Gifford Funds Services LLC, an affiliate of Baillie Gifford Overseas Limited and a member of FINRA.

Dating back to 1371, the Worshipful Company of Haberdashers has few worldwide equals for business longevity. Haberdashers’ Hall, home of the ancient City of London livery company, was thus an appropriately long-termist backdrop to Baillie Gifford’s Global Alpha Investor Forum.

It was recent history that was top of mind for the Strategy’s three portfolio managers, Malcolm MacColl, Spencer Adair and Helen Xiong, who acknowledged that the last three years have been tough for clients and investors. Reflecting on this period, the managers said they have sought out situations where they could have acted differently and learned lessons from this process.

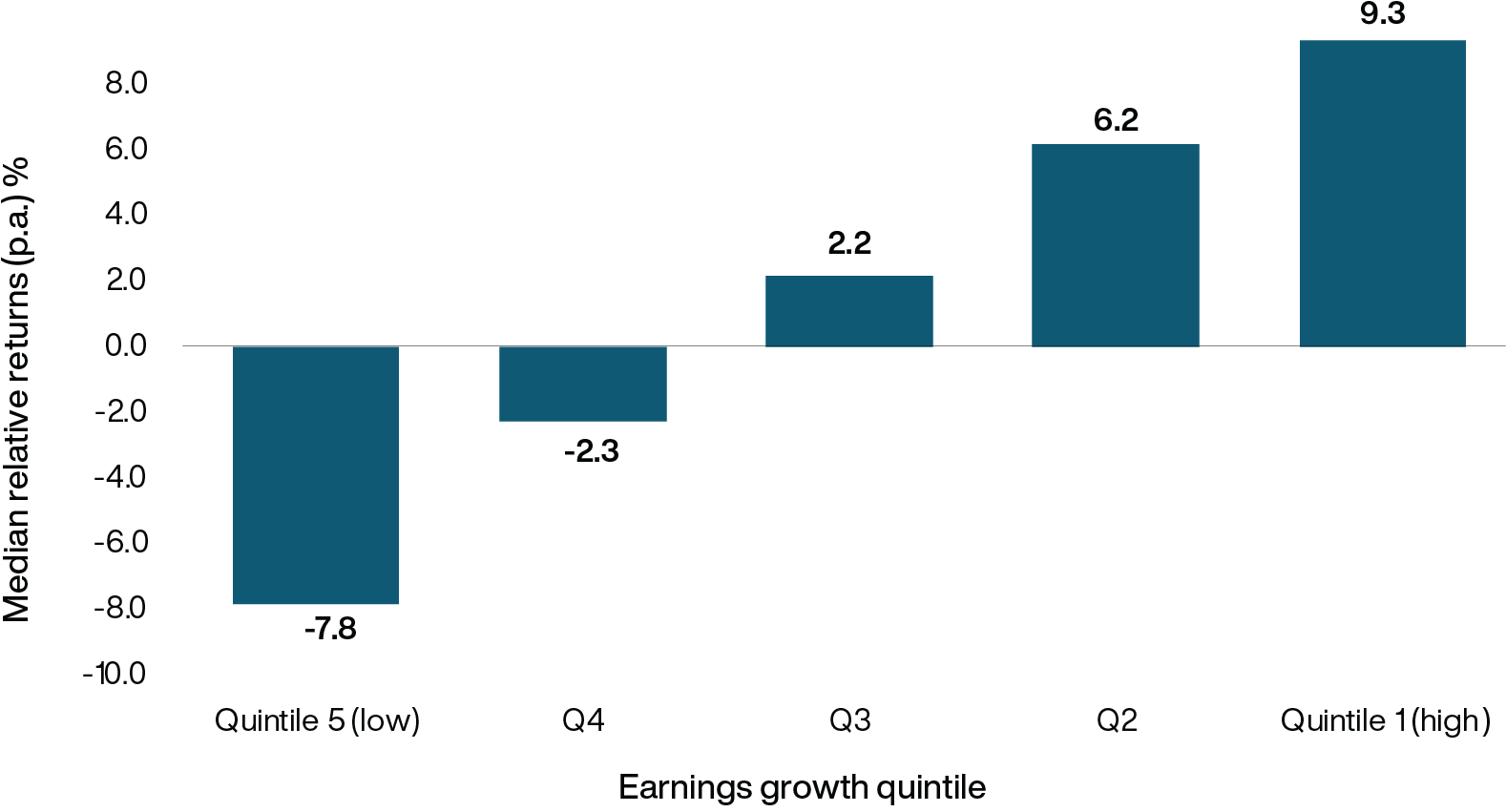

Malcolm MacColl emphasised that the team remains strongly committed to Global Alpha’s reward-seeking growth philosophy, reiterating his faith in the power of compounding as a means of generating long-term wealth. Citing independent data, he showed the correlation between higher earnings growth rates and higher excess returns for stocks. He highlighted how the rolling five-year returns of the top 20 per cent of companies in terms of earnings growth have outperformed the wider market by over 9 per cent over the last 34 years.

The case for long-term growth investing

Five-year returns by five-year earnings growth quintile

Rolling five-year horizons (1989-2023)

Source: FactSet, MSCI, FTSE. US dollar.

The universe consists of all stocks listed in the FTSE World and MSCI ACWI Indices at each starting point excluding repetitions.

Date range: 31 December 1989 to 31 December 2023.

MacColl explained, “The underlying philosophy of our strategy is that growth works. The question then is whether the portfolio is invested in the right growth companies for our investors?”

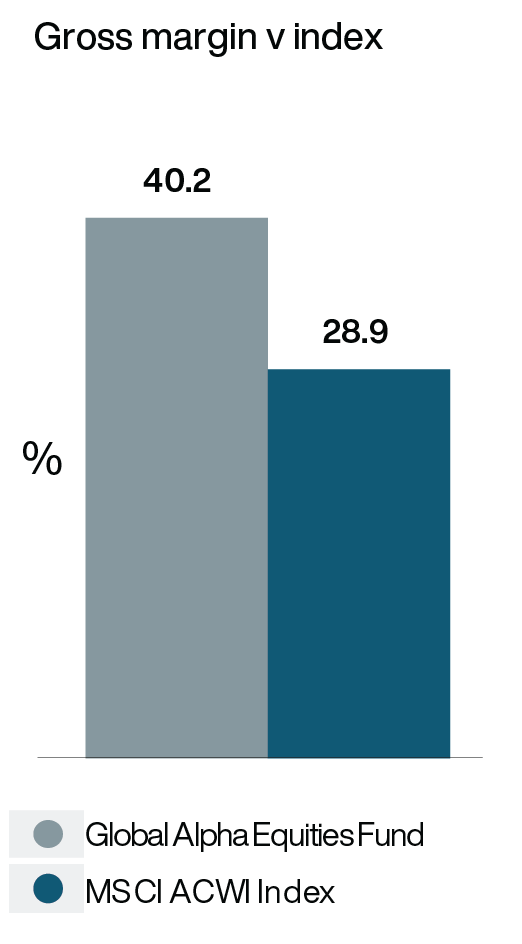

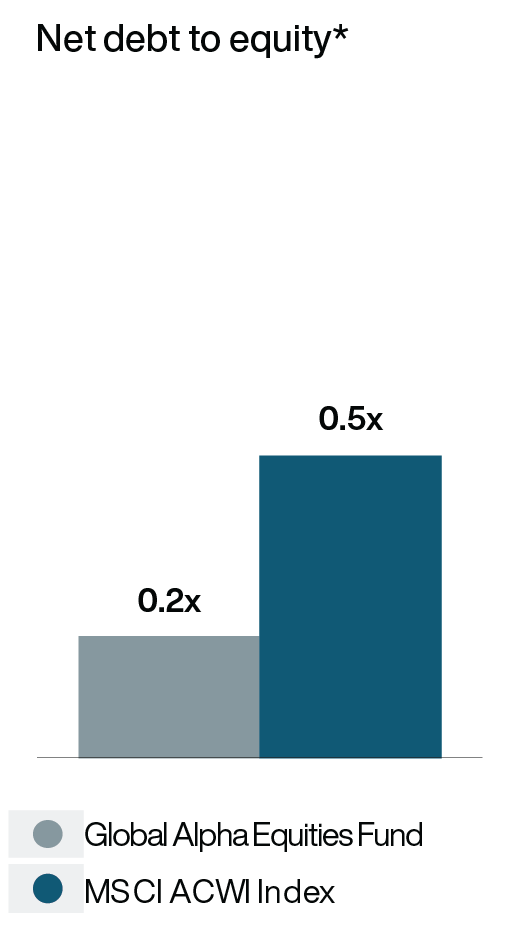

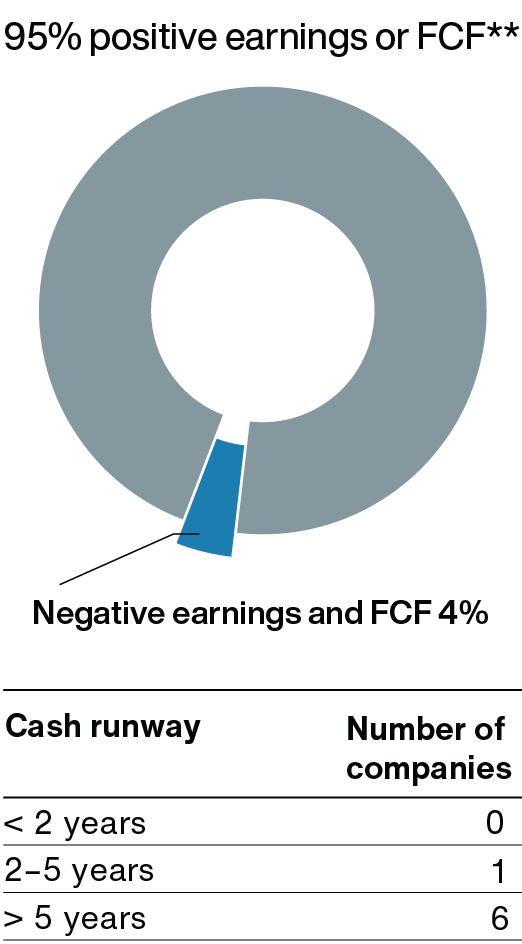

His detailed examination of the portfolio suggests that it is. For instance, the gross margins of the portfolio in aggregate are more than 10 per cent higher than the market average, while borrowings are considerably lower, and 95 per cent of portfolio companies being cash-flow-positive.

Portfolio strength

Source: Baillie Gifford & Co, FactSet, Revolution, MSCI. Richemont do not make this data available therefore are excluded from earnings data. Holding weight is 1.1%. As at 31 December 2023, USD.

*The debt-to-equity (D/E) ratio is a leverage ratio, which shows how much of a company's financing or capital structure is made up of debt versus issuing shares of equity. Presented as a ratio.

Fund and index net debt to equity figures excludes financials. Fund and index earnings figures are calculated excluding negative earnings.

**Free cash flow (FCF) is a company's available cash repaid to creditors and as dividends and interest to investors.

However, the level of growth from these companies is more critical. Data from FactSet shows the portfolio’s companies in aggregate are forecast to grow two and a half times faster than the market over the next three years.

Following a period of unexpected volatility, MacColl and colleagues stressed that the portfolio is well positioned for an environment where, even if interest rates or inflation stay high, the companies are likely to do well.

Enduring growth

This might seem surprising, given that the background is not particularly encouraging – decelerating global growth, the threat of a US recession and rising geopolitical tensions. In her remarks, Helen Xiong pointed out that aside from any short-term implications the correlation between adverse events and share prices over the long term is tenuous at best.

“Since the 1920s, the US has had around 17 recessions, including the Great Depression, numerous wars and now also a global pandemic. Yet over the last 100 years, the S&P has delivered around 10 per cent per annum” she said.

In any case, she added, present high interest rates matter little to companies with a low level of debt, while companies who are cash positive will be able to fund their own growth. Regardless of geopolitical and economic events, these companies are capable of delivering high earnings growth, which is what drives share prices over the long term.

Xiong quoted the economist and ‘creative destruction’ theorist Joseph Schumpeter, who noted that the fundamental impulse of capitalism comes from new goods, new methods of production or transport, new markets, and different kinds of organisations. Xiong cited the success of DoorDash. Its strong balance sheet has helped to fund acquisitions, which have led to the company winning a two-thirds share of the US food delivery market.

Another illustration from the portfolio of the disruptive benefits of applying new technology to old businesses is the growth of ‘programmatic’ or tailored digital advertising service The Trade Desk, which has outstripped traditional advertisers.

A major theme of the evening was that, while volatility can be trying for investors, it can also be an opportunity. Over the last year, the Global Alpha portfolio managers have been reducing the position sizes of companies in the portfolio whose value has held up well. They are also taking advantage of the opportunity to invest in companies whose share prices appear unjustifiably low, such as Texas Instruments, one of the world’s largest semiconductor makers.

Long-term opportunity

In his remarks, Spencer Adair reminded us of how badly market sentiment, like clothing fads, can date. Who now would return to the 1980s, when shoulder pads ruled supreme? His point was that that the stock market can be as fickle as the high street. Sometimes returns outstrip fundamentals while, as in recent times, strong fundamentals have not sustained share prices. These, he said, are like coiled springs, waiting to spring back to normality.

Adair used share price data from around the Global Financial Crisis (GFC) to make his point about how quickly things can bounce back. His experience is that over time, share prices follow fundamentals, which drive long-term returns. “We think we are at a similar point to when things began to inflect upwards after the GFC. It’s not something we can prove with data, but we’re confident,” he said.

Underpinning that belief is the pace of earnings growth, which has seen a sharp acceleration. “We're seeing companies that are already growing suddenly accelerate even further,” he added. “They’ve been running at a certain pace and then the pace increases. For example, the shift to cloud and AI has meant that Microsoft grew its earnings 33 per cent last quarter. That shouldn't happen to a 48-year-old company. It shouldn't happen to a $3tn company.”

Similar success can be seen in semiconductor companies in the portfolio such as TSMC, as well as in companies that are fixing worn-out infrastructure or adapting to changing climate conditions. One example is Advanced Drainage Systems, which makes super-lightweight and durable storm drains that are easier to install than conventional ones and could last for a century. It is seeing a sharp acceleration in earnings.

So too is Comfort Systems, which provides skilled air conditioning and electrical engineers to help fit out and upgrade large commercial buildings. Skilled construction labour is at a real shortage in the US and so business is booming. Comfort Systems grew earnings 65 per cent last quarter.

Talking of fashion, the managers noted how some of the deeper trends underpinning their investment philosophy have fallen out of favour. Healthcare is a good example. As society ages, healthcare revenues will grow, yet the industry had its worst year in two decades last year. While healthcare stocks have been trading at a 10-year low relative to the wider market, the managers have been slowly building up holdings in companies such as US health insurance provider Elevance Health, trading on just 13 times earnings in a market whose prospects are buoyed by an ageing population requiring more healthcare.

Demographics also favour emerging markets, yet, as Adair noted, these too have rarely been so unfashionable. Many technology companies in South Korea, China and Brazil are world-class, capitalising on strong business models. Several of these are, in the managers’ view, superior companies trading at very big discounts to their western peers. The companies are responding to this and taking on multinational competitors closer to home.

In the developed world, too, Global Alpha holdings such as Meta and Spotify are quietly flourishing, with strong operating momentum and improving profitability. Taken as a whole, the managers see plentiful signs of growth inflecting upwards and good reasons to believe the Global Alpha portfolio is well placed for the future.

Generative AI: the next frontier

What are the implications and potential for generative Artificial Intelligence (AI)? The question was explored in a breakout session with Malcolm MacColl, Helen Xiong and Global Alpha investment analyst Jacob Teal.

AI’s ability to process data and speak to humans has captured the world’s attention in just a year, but this is only the beginning of a far wider transformation. Many of the firms whose services are part of everyday life such as Spotify, Netflix or Meta are essentially software companies using algorithms. Generative AI is not a new algorithm but a new paradigm, a new way to develop software through training rather than coding.

Explained Jacob Teal: “These systems can tell patterns from information that already exists and can create new information from patterns that they've learned. That's what's new. It is even more exciting because the right hardware to enable the software is coming through at just the right time.”

Potential applications extend well beyond ChatGPT to applications including artwork, music, protein synthesis and software development. “There is no limit to where generative AI could go or to how intelligent systems can be in their ability to understand human context, which means the potential for its application is very wide,” Helen Xiong said.

In terms of what it means for companies in the portfolio, MacColl explained that the managers need to think through the implications of AI in all its different forms. “We need to understand how it can be deployed to improve efficiency or increase research and development and so on. We also need to be aware of where it can be an undermining force and perhaps change business models or disrupt incumbents.”

Repair, renew, revitalise: the infrastructure opportunity

Client Director Jon Henry introduced Spencer Adair, Mike Taylor – one of the North America scouts for Global Alpha – and Kieran Murray, Global Alpha’s environmental, social and governance (ESG) analyst, to discuss the opportunities arising from the need to urgently upgrade much of the world’s infrastructure and deal with climate change. About one-fifth of the portfolio is invested along the theme of ‘repair, renew and revitalise’.

“Most of the infrastructure in the western world was put in place in the period after World War Two in the 40s, 50s and 60s,” Adair began. “Infrastructure as a proportion of GDP peaked in the early 70s and has been declining since.

Adapting to harsher climate conditions also requires better drainage for storms, higher sea walls and breaks for forest fires. Governments and companies are increasingly aware of geopolitical tensions and threats to integrated global supply chains. Countries need to make their own vaccines, pharmaceuticals and semiconductors. The stimulus beginning to come through is unprecedented, particularly the $2.2tn committed by the US legislature to upgrade domestic infrastructure, equivalent in today’s values to about 13 post-World War Two Marshall Plans.

Increasing investment in infrastructure is beginning to come through to companies in this area. Although building materials and solutions provider CRH has enjoyed about 15 per cent growth a year for the last 50 years, it now says that it is entering a period of golden growth.

“These companies are outwardly boring, and that’s why we like them,” added Taylor. “They’re frequently well-managed, often run by families who build up their businesses in a niche area. An outwardly dull façade can mask an excellent competitive position.”

Risk factors

This content contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research and Baillie Gifford and its staff may have dealt in the investments concerned.

As with all mutual funds, the value of an investment in the fund could decline, so you could lose money.

The most significant risks of an investment in the Baillie Gifford Global Alpha Equities Fund are Investment Style Risk, Growth Stock Risk, Long-Term Investment Strategy Risk and Non-U.S. Investment Risk. The Fund is managed on a bottom up basis and stock selection is likely to be the main driver of investment returns. Returns are unlikely to track the movements of the benchmark. The prices of growth stocks can be based largely on expectations of future earnings and can decline significantly in reaction to negative news. The Fund is managed on a long-term outlook, meaning that the Fund managers look for investments that they think will make returns over a number of years, rather than over shorter time periods. Non-U.S. securities are subject to additional risks, including less liquidity, increased volatility, less transparency, withholding or other taxes and increased vulnerability to adverse changes in local and global economic conditions. There can be less regulation and possible fluctuation in value due to adverse political conditions. Other Fund risks include: Asia Risk, China Risk, Conflicts of Interest Risk, Currency Risk, Emerging Markets Risk, Equity Securities Risk, Environmental, Social and Governance Risk, Focused Investment Risk, Government and Regulatory Risk, Information Technology Risk, Initial Public Offering Risk, Large-Capitalization Securities Risk, Liquidity Risk, Market Disruption and Geopolitical Risk, Market Risk, Service Provider Risk, Settlement Risk, Small-and Medium-Capitalization Securities Risk and Valuation Risk.

For more information about these and other risks of an investment in the fund, see “Principal Investment Risks” and “Additional Investment Strategies” in the prospectus. The Baillie Gifford Global Alpha Equities Fund seeks capital appreciation. There can be no assurance, however, that the fund will achieve its investment objective.

The fund is distributed by Baillie Gifford Funds Services LLC. Baillie Gifford Funds Services LLC is registered as a broker-dealer with the SEC, a member of FINRA and is an affiliate of Baillie Gifford Overseas Limited.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this article are for illustrative purposes only.

The Baillie Gifford Global Alpha Equities Fund

(Share Class K) as of December 31, 2023

|

Gross Expense Ratio |

0.67% |

|

Net Expense Ratio |

0.67% |

Source: Baillie Gifford & Co

Annualised total return as of December 31, 2023 (%)

| 1 year | 3 years | 5 years | 10 years | |

|

The Baillie Gifford Global Alpha Equities Fund |

19.65 |

-2.99 |

10.53 |

8.42 |

|

MSCI All Country World Index |

22.81 |

6.26 |

12.28 |

8.48 |

Source: Bank of New York Mellon, MSCI. NAV returns in US dollars.

The performance data quoted represents past performance and is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end performance please visit our website at bailliegifford.com/usmutualfunds.

Returns are based on the K share class from April 28, 2017. Prior to that date returns are calculated based on the oldest share class of the Fund adjusted to reflect the K share class fees where these fees are higher.

Baillie Gifford fund’s performance shown assumes the reinvestment of dividend and capital gain distributions and is net of management fees and expenses. Returns for periods less than one year are not annualised. From time to time, certain fees and/or expenses have been voluntarily or contractually waived or reimbursed, which has resulted in higher returns. Without these waivers or reimbursements, the returns would have been lower. Voluntary waivers or reimbursements may be applied or discontinued at any time without notice. Only the Board of Trustees may modify or terminate contractual fee waivers or expense reimbursements. Fees and expenses apply to a continued investment in the funds. All fees are described in each fund’s current prospectus.

Expense Ratios: All mutual funds have expense ratios which represent what shareholders pay for operating expenses and management fees. Expense ratios are expressed as an annualized percentage of a fund’s average net assets paid out in expenses. Expense ratio information is as of the fund’s current prospectus, as revised and supplemented from time to time. The net expense ratios for this fund are contractually capped (excluding taxes, sub-accounting expenses and extraordinary expenses), through April 30, 2024.

The MSCI All Country World is a free float-adjusted market capitalization weighted index that is designed to measure equity market performance in the global developed and emerging markets, excluding the United States. This unmanaged index does not reflect fees and expenses and is not available for direct investment.

Top Ten Holdings to December 31, 2023

|

Holdings |

Fund % |

|

1. Microsoft |

3.70 |

|

2. Martin Marietta Materials |

3.51 |

|

3. Amazon |

3.40 |

|

4. Elevance Health |

3.31 |

|

5. Moody's |

3.29 |

|

6. Ryanair |

3.07 |

|

7. CRH |

2.80 |

|

8. Meta |

2.72 |

|

9. Alphabet |

2.47 |

|

10. Reliance Industries |

2.35 |

It should not be assumed that recommendations/transactions made in the future will be profitable or will equal performance of the securities mentioned. A full list of holdings is available on request. The composition of the fund's holdings is subject to change. Percentages are based on securities at market value.

93048 10045873