Key points

- Portfolio companies demonstrate adaptability, pricing power and innovation, setting a strong course for future growth

- Monks looks beyond the obvious to capture unrecognised long-term growth opportunities

- With its broad perspective on growth, Monks has crafted a diverse portfolio poised for long-term success

Your capital may be at risk

The past year in financial markets is best described as a ‘game of two halves’. The first was a cagey and nervous affair. The dominant narrative was uncertainty about the prospect of a US recession. The second was much more encouraging. Similarly, the second half of Monks’ financial year delivered markedly stronger results than the first. A net asset value (NAV) total return of +21.6 per cent (the index delivered +16.6 per cent) compares strongly to the -3.3 per cent registered in the first half of the year.

Against a backdrop of growing optimism as inflation stabilised and central banks paused interest rate increases, investors continued to recognise the transformational potential of artificial intelligence (AI). This manifested most obviously in the share prices of some of the world’s largest technology stocks (several of which we own within Monks). Equity indices rallied, driven by these companies and, in some cases, hit new highs.

Performance

We recently released our annual report and accounts. In the twelve months to the end of April, the portfolio underperformed the comparative index (FTSE World) by 1.5 per cent, delivering a NAV total return of 17.6 per cent (share price 19.1 per cent), against the index total return of 19.1 per cent.

Our insurance and healthcare holdings were among the largest detractors from relative performance. The share prices of AIA, Ping An and Prudential (totalling 3 per cent of the portfolio) fell by an average of 34 per cent in the period.

The lingering effect of the pandemic on the Chinese economy curtailed active selling opportunities (as salesforce activity remains below pre-pandemic levels) and weakened consumer demand. We have sold our positions in Ping An and Prudential. We believe AIA is best placed to take advantage of the significant structural long-term growth opportunity that remains in China and across Asia more broadly, where the ‘protection gap’ in insurance coverage is large.

The healthcare sector is navigating a challenging period against a backdrop of excess inventory build-up following the pandemic, which suppressed demand, and a much more difficult funding environment for drug developers. In relation to the latter, we believe this supports our position in Royalty Pharma, a provider of capital to late-stage drug developers. While its share price has been weak, down 20 per cent in the year, we continue to believe that operational progress is on track.

We have sold Novocure (cancer treatment). Our central expectation was that it could successfully expand its addressable market by applying its tumour treatment field technology, designed to treat solid-state brain tumours, to instances affecting other vital organs. Setbacks in recent clinical trials have negatively impacted the probabilities of success and weakened our conviction in the investment case.

In contrast, most portfolio holdings are adapting and executing well. Several have proven their adaptability by exerting exceptional pricing power and have been the strongest positive contributors to portfolio return. Martin Marietta (aggregates and building supplies) is a case in point. It has been able to increase aggregate pricing significantly (14 per cent year-over-year) and deliver record levels of profitability.

It has been a similar story at CRH (cement and building supplies), which was the second-largest contributor to portfolio return.

Elsewhere, Meta (social media) as one of our Stalwart growth holdings, has unleashed the power of its advertising estate by leveraging its growing AI capabilities to improve its utility to merchants. This has driven demand for its advertising capacity and gradually improved pricing. In conjunction with sensible cost control and more disciplined growth spending, Meta has delivered a doubling of net income (up 117 per cent) year-over-year.

Others have executed flawlessly. Rapid growth holding DoorDash, the leading US food delivery platform, was the third largest positive contributor to portfolio returns. The company's commitment to improving its offerings for consumers, merchants, and delivery riders (known as 'dashers’) has propelled monthly active users to a record high, alongside a significant increase in average order frequency.

It now has almost two-thirds of the online meal delivery market in the US and grew revenues at 23 per cent year-over-year. DoorDash is making strong progress in new markets too, including online grocery delivery, as it seeks to become the convenience platform of choice for US consumers.

Innovation beyond the obvious

While markets have been narrowly focused over the past year, we have continued to embrace a wide array of opportunities. These span both digital and physical spheres – from enterprise cloud computing and digital payments to telegraph poles and HVAC (heating, ventilation, and air conditioning) installation. We expect market returns to broaden over time. The Monks portfolio should benefit as it aligns with deep structural trends that will support long-term growth.

Below are some of these structural trends and related changes to the portfolio over the last year:

- Digital payments: the market has developed hugely since the first consumer payment was recorded in 1994 (a CD copy of Sting’s Ten Summoner’s Tales for $12.48 on NetMarket, for trivia fans). Indeed, the value of global digital payment transactions has doubled (to over $6tn) in the past five years alone and there remains much to go for.

We have purchased a new position in Block which owns Cash App, the most popular finance application in the US with over 80 million users. Started as a peer-to-peer payments application, it has developed into a fully-fledged consumer app, offering multiple services.

The other part of its offering is its Square point-of-sale hardware, which enables merchants – often small- or micro-businesses without an online presence – to accept digital payments. It is a simple, convenient, and easy-to-use solution for merchants to accept a wide variety of digital payments.

The portfolio has exposure to a range of other digital payment businesses, including Mastercard, the rapidly growing MercadoPago (operated by MercadoLibre) in South America, and Adyen, the Dutch payments business, to which we added in the period.

- Semiconductors: technological advancements in semiconductors are driving the exponential acceleration of computing power. This has potentially profound implications for what ‘computers’ can do in the future, from driving cars autonomously (at scale), to producing music, content and independently writing code.

We have deliberately grown the portfolio’s exposure to the semiconductor industry (now 10 per cent of the portfolio) over the past couple of years. In our interim report, we underlined our enthusiasm for the purchase of NVIDIA as the leading global designer of graphics processing units (GPUs), a key enabler of artificial intelligence (AI) applications.

In recent months, we have added holdings in semiconductor companies Texas Instruments and Samsung Electronics. Growth in both cases will be driven by secular trends towards greater electrification, for example, in the automotive market, the use of consumer electronics (think smartphones, laptops, and tablets), and the ongoing build-out of data centres to support increasing cloud computing capacity.

- Healthcare: the long-term drivers of an increasing need for healthcare are clear. The global population of over-60s will double by 2050. The number of over-80s will triple. As we age, we ‘consume’ much more healthcare.

We added a position in the Danish insulin business, Novo Nordisk. It has seen a recent rapid transformation from a steadily compounding business focusing on diabetes care and clotting, to leading the way in GLP-1 weight-loss drugs. Novo's drug, WeGovy, has opened a huge, global market and is addressing obesity, one of the world's biggest health challenges.

The opportunity could reach hundreds of millions who are clinically obese, unlocking further opportunities by reducing the long list of health complications that come with the condition (heart disease, cancers, liver disease etc).

- Infrastructure: we have continued to invest where companies may benefit from a planned infrastructure upgrade, particularly in the US. There are several factors, including 're-shoring' trends and infrastructure spending (supported by legislation such as President Biden's Inflation Reduction Act), which are likely to support a material uptick in capital spending on areas including roads, energy, and digital networks.

In our interim update, we wrote about our enthusiasm for Comfort Systems, the HVAC installer and we recently established a position in the Canadian company Stella-Jones. It is North America's largest manufacturer of pressure-treated wood products.

The growth case rests on its core product, wooden utility poles, used for electrical and communications infrastructure. For the US to decarbonise its energy systems and have a chance of achieving its net zero ambitions, it will need substantial investment in its national power grid. We believe volume growth and pricing power will boost profitability in the coming years.

Outlook

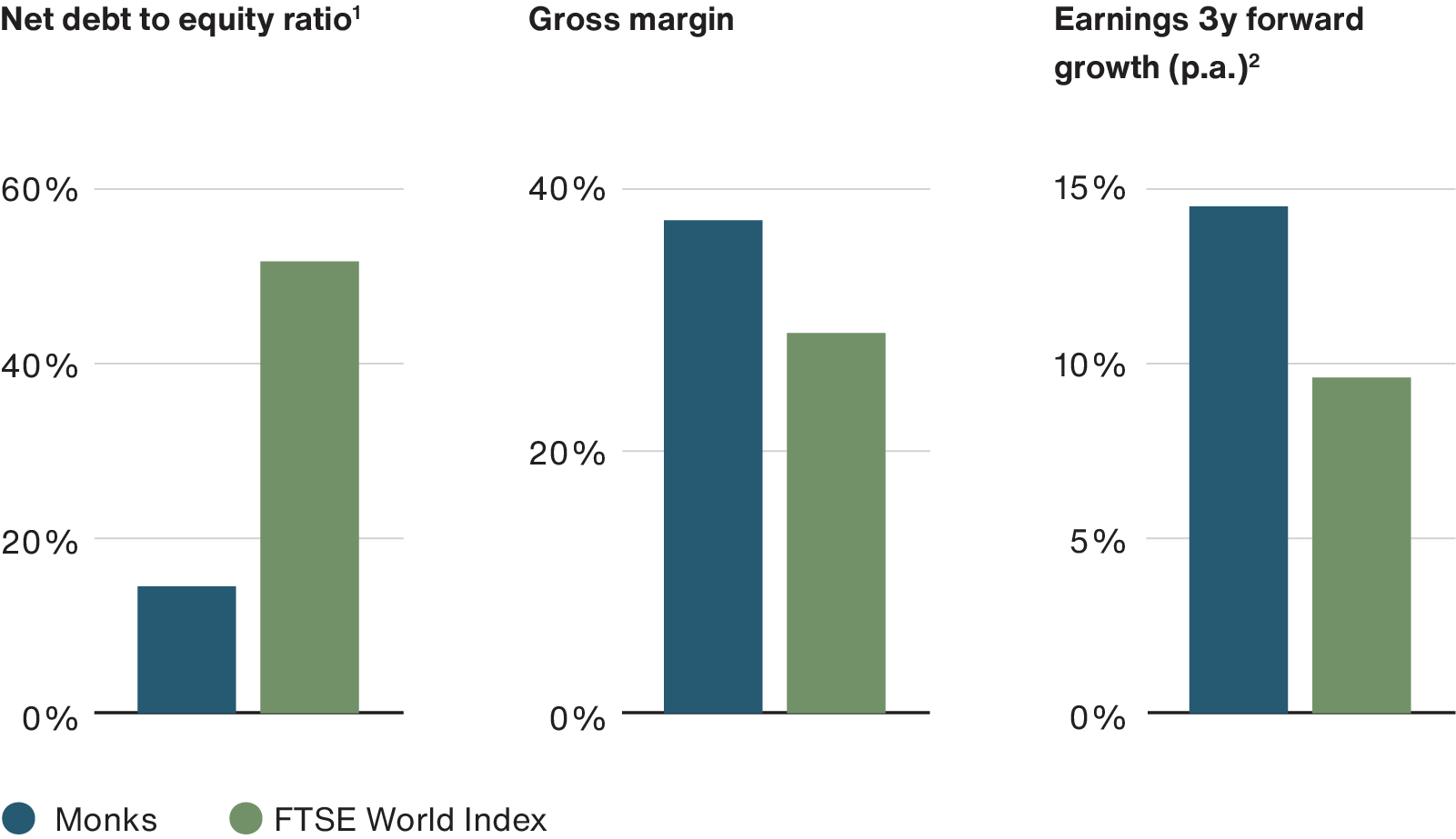

Across our portfolio companies are operating well while continuing to invest for the future. This has translated into strong delivered and forecast earnings growth.

Source: Bailie Gifford & Co, FactSet, FTSE. Sterling. As at 30 April 2024. Based on The Monks Investment Trust PLC.

1Excludes financials. Totals may not sum due to rounding. 2Excludes companies with negative earnings.

Encouragingly, there are signs that investment markets, against a backdrop of stabilising inflation and interest rates, are more willing to recognise this. Relative performance has begun to rebound strongly.

Our optimism is reflected in our decision to raise medium-term debt (£73m) in the private placement market (net gearing was 6.8 per cent at year-end). Our blended cost of borrowing is now 2.74 per cent, a low hurdle when set against future investment opportunities.

As we look ahead, what is most exciting is that the rate of change and technological development is accelerating. It underpins a growing, often underappreciated, opportunity set. By our willingness to take a wide-angled view of growth (defined by our growth profiles – Stalwart, Rapid and Cyclical), we have the latitude to invest beyond the obvious. This allows us to harness the potential of lesser-known but nevertheless exceptional growth companies.

Our portfolio reflects an eclectic and growing opportunity set. We’re confident that it will deliver for shareholders in the years ahead.

| 2020 | 2021 | 2022 | 2023 | 2024 | |

| Monks Ord | 15.3 | 30.2 | -32.1 | 6.8 | 19.6 |

| Monks NAV | 17.0 | 37.2 | -26.8 | 9.1 | 17.9 |

| FTSE World Index | 5.8 | 25.5 | -2.8 | 13.5 | 21.1 |

Performance source: Morningstar, FTSE, total return in sterling

Past performance is not a guide to future returns.

Important information

This communication was produced and approved in July 2024 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

The Trust invests in overseas securities. Changes in the rates of exchange may also cause the value of your investment (and any income it may pay) to go down or up.

This article does not constitute, and is not subject to the protections afforded to, independent research. Baillie Gifford and its staff may have dealt in the investments concerned. The views expressed are not statements of fact and should not be considered as advice or a recommendation to buy, sell or hold a particular investment.

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). The investment trusts managed by Baillie Gifford & Co Limited are listed on the London Stock Exchange and are not authorised or regulated by the FCA.

A Key Information Document is available at bailliegifford.com.

FTSE index data

Source: London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2023. FTSE Russell is a trading name of certain of the LSE Group companies. “FTSE®” “Russell®”, “FTSE Russell ®, is/are a trade mark(s) of the relevant LSE Group companies and is/are used by any other LSE Group company under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication.

112603 10048903