The Power Law is Sebastian Mallaby's fifth book

Please remember that the value of an investment can fall and you may not get back the amount invested.

The heroes of American ‘big tech’, those who get kudos for its extraordinary success, are the founder-leaders – the likes of Jeff Bezos, Mark Zuckerberg and Elon Musk. Sebastian Mallaby argues that their early backers also deserve much of the credit.

We meet in central London, where Mallaby is taking part in a Baillie Gifford clients event themed on private company investment opportunities. He recently wrote The Power Law: Venture Capital and the Art of Disruption and is there to share his expertise on the role VC firms play in the broader private markets ecosystem, in which Baillie Gifford is active.

The ‘power law’ of the book’s title is also called the Pareto principle and is based on the idea there is an 80-to-20 precept at work in the universe. For example:

- 20 per cent of the population owns 80 per cent of the money

- 20 per cent of a business’s customers typically account for 80 per cent of its profits

- 20 per cent of drivers cause 80 per cent of traffic accidents

The actual numbers may not be pinpoint precise, but the general ratio holds true.

Mallaby explains that Silicon Valley ‘adventure capitalists’ know the distribution of their returns from investing in startups obeys the power law. Most will fail completely.

“But,” he adds, “each year brings a handful of outliers that hit the proverbial grand slam, and the only thing that matters in venture is to own a piece of them.” For venture capitalists, that means making audacious private bets on companies, often without a track record on which to judge them.

Mallaby grew up in Britain before moving to Washington, DC to work for The Economist and later The Washington Post. His previous books include an account of James Wolfensohn’s time as the World Bank’s president, a prize-winning biography of Federal Reserve chairman Alan Greenspan, and a history of the hedge fund industry.

For a his latest take on modern financial history, he sought to explore an asset class that he says was rising in importance but underexplained.

“I thought venture capital was the most exciting part of private markets,” Mallaby tells me.

“But I felt as if it was very opaque. There was a mystery story that had to be unravelled.” So, he organised some introductions from friends and colleagues and went to Silicon Valley.

Investing with intuition

Once there, Mallaby quickly sensed that the venture guys (and they were mostly men) invested in people as much as technology. The most original would-be entrepreneurs tended to be the most difficult characters – “arrogant, misanthropic or borderline crazy”, in one memorable phrase.

Valley investors are on the lookout for evidence of staying power and “immigrant grit”, as Michael Moritz, former chief of VC firm Sequoia Capital, once put it, often having a preference for entrepreneurs born outside the US.

They also network relentlessly, cooperating and sharing ideas rather than hoarding them. “Network entrenchment, which gives you deal flow, is one thing that differentiates very successful venture capitalists from the rest,” Mallaby comments.

Other types of investors also back private companies. But venture capital does it early and when there is high risk involved, often using money raised from large institutions such as sovereign wealth funds, family offices and trusts. (Members of the public typically can’t invest directly.)

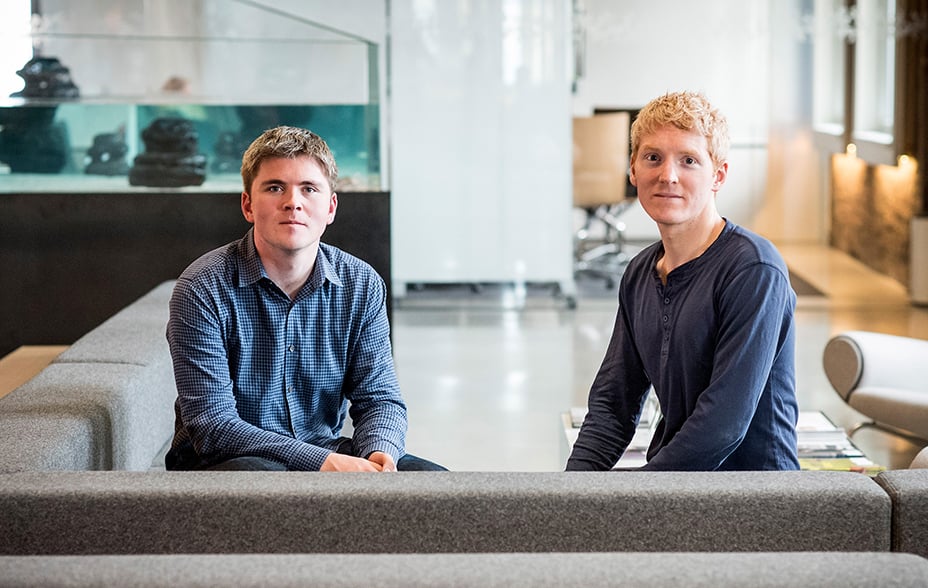

For example, the payment company Stripe attracted ‘seed’ investment from Valley venture firms Sequoia Capital, Andreessen Horowitz and SV Angel just months after its founders Patrick and John Collison had committed to it full-time in 2010. And Sequoia followed this with further capital over subsequent funding rounds.

Stripe co-founders John Collison (left) and Patrick Collison (right)

©Bloomberg/Getty Images

The Collison brothers ticked a lot of venture boxes. They were immigrants from Ireland (tick). They had already launched and sold another business (tick). Their technology had a large target market with natural protection against competitors (tick).

The Collisons think they ticked another box (“pluck”) when Sequoia’s Michael Moritz learned Patrick cycled everywhere and clocked a keen time on a tough local hill climb. Sequoia was alerted early on to the Collisons thanks to its assiduous networking. One of the scouts who tipped off the venture firm was Sam Altman, later chief executive of artificial intelligence researcher OpenAI.

Mallaby notes that by 2021, Stripe was valued at $95bn and Sequoia’s stake $15bn. Baillie Gifford first invested in Stripe, now one of its largest private holdings, in 2019.

Manufacturing courage

Openness, aggression and belief in the power law distinguish Silicon Valley from the other home of US venture capital, the more secretive Boston, Mallaby suggests. And that helped give the west coast variant the upper hand in the 1980s.

Mallaby recalls a Boston venture capitalist who boasted that only two of his 40 investments had lost money. “If you said that in California, they would think you were an idiot,” he says. “Silicon Valley thinks failure is a learning experience and is willing to give you a second shot.”

Early Silicon Valley venture deals centred on capital-intensive industries, including silicon chips and other electronics hardware. Then, the focus shifted to less capital-intensive code. “Software is eating the world,” as Valley investor Marc Andreessen put it.

Some venture software successes were epic. Sequoia and Kleiner Perkins each invested $12m for 12.5 per cent of Google in 1999. When it floated in 2004, the search firm was worth $23bn.

Kleiner Perkins performed another service, which became part of venture capital’s repertoire, by persuading experienced businessman Eric Schmidt to become chief executive. It did this by promising him if the move didn’t work out, it would find him an equally good job elsewhere in the Valley.

“They derisked the decision to start the company, and then they derisked Schmidt’s decision to join,” Mallaby says. “Venture capital is a machine that manufactures courage for entrepreneurs.”

Entrepreneurial evolution

Some entrepreneurs went from courting the leading venture capitalists to disdaining them – calling them “greedy” and “overbearing”. Mallaby tells of how Facebook’s Mark Zuckerberg turned up late for a meeting with Sequoia in 2004, wearing pyjama bottoms and with a slide deck of 10 reasons why the VC firm shouldn’t invest in his company.

One of Zuckerberg’s partners had previously fallen out with Sequoia, so he had no intention of accepting its investment. Facebook could do this because sources of capital had diversified with the arrival of more venture capital firms and ‘angel backers’ – successful entrepreneurs supporting other startups.

Mallaby says that trend accelerated after the 2008 financial crisis, once regulators restricted Wall Street’s public trading profits. Over the following decade, he notes the number of US venture investors more than doubled, as did the number of startups they backed.

Other later-stage investors have also become involved. That has allowed private companies to stay private longer, focusing on their long-term goals rather than quarterly financial reports. However, Mallaby raises concerns as to whether this sometimes leads to less external oversight of the firms’ management.

“If you care about your returns, across a whole bunch of these growth companies, you probably want the sector as a whole to have better corporate governance. So, I think there is a discussion [to be had],” he says.

And indeed, this was one of the topics later covered at the clients event in the context of Baillie Gifford’s own focus on the importance of high-quality conversations and other engagements with its holdings.

AI and biotech

While private markets flourished during the low interest rate years, higher rates have done them no favours. Mallaby thinks this needs to be put into perspective, however.

“For venture capital, the prospects for a particular technology are much more important than the cost of money,” he insists. “Innovation and disruption can massively outpace anything as mundane as higher interest rates.”

Disruptive companies will continue to be the story of the future, he suggests, as artificial intelligence develops and biotech gets even more exciting.

“Technology is going to remain the exciting story in how you generate growth,” Mallaby concludes.

“It’s not going to be leverage, it's not going to be globalisation. It's going to be tech.”

Risk factors

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in February 2024 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Investing in private companies could increase risk as these assets may be more difficult to sell, so changes in their prices may be greater.

Potential for profit and loss

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk. Past performance is not a guide to future returns.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.

Important Information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

Baillie Gifford Overseas Limited provides investment management and advisory services to non-UK Professional/Institutional clients only. Baillie Gifford Overseas Limited is wholly owned by Baillie Gifford & Co. Baillie Gifford & Co and Baillie Gifford Overseas Limited are authorised and regulated by the FCA in the UK.

Persons resident or domiciled outside the UK should consult with their professional advisers as to whether they require any governmental or other consents in order to enable them to invest, and with their tax advisers for advice relevant to their own particular circumstances.

Financial Intermediaries

This communication is suitable for use of financial intermediaries. Financial intermediaries are solely responsible for any further distribution and Baillie Gifford takes no responsibility for the reliance on this document by any other person who did not receive this document directly from Baillie Gifford.

Europe

Baillie Gifford Investment Management (Europe) Limited provides investment management and advisory services to European (excluding UK) clients. It was incorporated in Ireland in May 2018. Baillie Gifford Investment Management (Europe) Limited is authorised by the Central Bank of Ireland as an AIFM under the AIFM Regulations and as a UCITS management company under the UCITS Regulation. Baillie Gifford Investment Management (Europe) Limited is also authorised in accordance with Regulation 7 of the AIFM Regulations, to provide management of portfolios of investments, including Individual Portfolio Management (‘IPM’) and Non-Core Services. Baillie Gifford Investment Management (Europe) Limited has been appointed as UCITS management company to the following UCITS umbrella company; Baillie Gifford Worldwide Funds plc. Through passporting it has established Baillie Gifford Investment Management (Europe) Limited (Frankfurt Branch) to market its investment management and advisory services and distribute Baillie Gifford Worldwide Funds plc in Germany. Similarly, it has established Baillie Gifford Investment Management (Europe) Limited (Amsterdam Branch) to market its investment management and advisory services and distribute Baillie Gifford Worldwide Funds plc in The Netherlands. Baillie Gifford Investment Management (Europe) Limited also has a representative office in Zurich, Switzerland pursuant to Art. 58 of the Federal Act on Financial Institutions (“FinIA”). The representative office is authorised by the Swiss Financial Market Supervisory Authority (FINMA). The representative office does not constitute a branch and therefore does not have authority to commit Baillie Gifford Investment Management (Europe) Limited. Baillie Gifford Investment Management (Europe) Limited is a wholly owned subsidiary of Baillie Gifford Overseas Limited, which is wholly owned by Baillie Gifford & Co. Baillie Gifford Overseas Limited and Baillie Gifford & Co are authorised and regulated in the UK by the Financial Conduct Authority.

China

Baillie Gifford Investment Management (Shanghai) Limited

柏基投资管理(上海)有限公司(‘BGIMS’) is wholly owned by Baillie Gifford Overseas Limited and may provide investment research to the Baillie Gifford Group pursuant to applicable laws. BGIMS is incorporated in Shanghai in the People’s Republic of China (‘PRC’) as a wholly foreign-owned limited liability company with a unified social credit code of 91310000MA1FL6KQ30. BGIMS is a registered Private Fund Manager with the Asset Management Association of China (‘AMAC’) and manages private security investment fund in the PRC, with a registration code of P1071226.

Baillie Gifford Overseas Investment Fund Management (Shanghai) Limited

柏基海外投资基金管理(上海)有限公司(‘BGQS’) is a wholly owned subsidiary of BGIMS incorporated in Shanghai as a limited liability company with its unified social credit code of 91310000MA1FL7JFXQ. BGQS is a registered Private Fund Manager with AMAC with a registration code of P1071708. BGQS has been approved by Shanghai Municipal Financial Regulatory Bureau for the Qualified Domestic Limited Partners (QDLP) Pilot Program, under which it may raise funds from PRC investors for making overseas investments.

Hong Kong

Baillie Gifford Asia (Hong Kong) Limited

柏基亞洲(香港)有限公司 is wholly owned by Baillie Gifford Overseas Limited and holds a Type 1 and a Type 2 license from the Securities & Futures Commission of Hong Kong to market and distribute Baillie Gifford’s range of collective investment schemes to professional investors in Hong Kong. Baillie Gifford Asia (Hong Kong) Limited

柏基亞洲(香港)有限公司 can be contacted at Suites 2713-2715, Two International Finance Centre, 8 Finance Street, Central, Hong Kong. Telephone +852 3756 5700.

South Korea

Baillie Gifford Overseas Limited is licensed with the Financial Services Commission in South Korea as a cross border Discretionary Investment Manager and Non-discretionary Investment Adviser.

Japan

Mitsubishi UFJ Baillie Gifford Asset Management Limited (‘MUBGAM’) is a joint venture company between Mitsubishi UFJ Trust & Banking Corporation and Baillie Gifford Overseas Limited. MUBGAM is authorised and regulated by the Financial Conduct Authority.

Australia

Baillie Gifford Overseas Limited (ARBN 118 567 178) is registered as a foreign company under the Corporations Act 2001 (Cth) and holds Foreign Australian Financial Services Licence No 528911. This material is provided to you on the basis that you are a “wholesale client” within the meaning of section 761G of the Corporations Act 2001 (Cth) (“Corporations Act”). Please advise Baillie Gifford Overseas Limited immediately if you are not a wholesale client. In no circumstances may this material be made available to a “retail client” within the meaning of section 761G of the Corporations Act.

This material contains general information only. It does not take into account any person’s objectives, financial situation or needs.

South Africa

Baillie Gifford Overseas Limited is registered as a Foreign Financial Services Provider with the Financial Sector Conduct Authority in South Africa.

North America

Baillie Gifford International LLC is wholly owned by Baillie Gifford Overseas Limited; it was formed in Delaware in 2005 and is registered with the SEC. It is the legal entity through which Baillie Gifford Overseas Limited provides client service and marketing functions in North America. Baillie Gifford Overseas Limited is registered with the SEC in the United States of America.

The Manager is not resident in Canada, its head office and principal place of business is in Edinburgh, Scotland. Baillie Gifford Overseas Limited is regulated in Canada as a portfolio manager and exempt market dealer with the Ontario Securities Commission (‘OSC’). Its portfolio manager licence is currently passported into Alberta, Quebec, Saskatchewan, Manitoba and Newfoundland & Labrador whereas the exempt market dealer licence is passported across all Canadian provinces and territories. Baillie Gifford International LLC is regulated by the OSC as an exempt market and its licence is passported across all Canadian provinces and territories. Baillie Gifford Investment Management (Europe) Limited (‘BGE’) relies on the International Investment Fund Manager Exemption in the provinces of Ontario and Quebec.

Israel

Baillie Gifford Overseas Limited is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the Advice Law) and does not carry insurance pursuant to the Advice Law. This material is only intended for those categories of Israeli residents who are qualified clients listed on the First Addendum to the Advice Law.

93122 10045562