Key points

- The Multi Asset Team expects economic growth to be resilient and inflation to fall towards central bank targets

- A higher neutral interest rate and strong equity performance this year have made equity markets less attractive

- Core and renewable energy infrastructure are among the best opportunities, alongside logistics-related real estate

All investment strategies have the potential for profit and loss, your or your clients capital may be at risk.

Inflation in the first half of 2024 proved quite volatile, with the first quarter seeing inflation rise quite significantly, particularly in the US, before rolling over in the second quarter. Although this volatility forced a few central banks to dial back their expectations for cutting interest rates, many developed countries have now started to lower their interest rates from post-Covid highs. For most of these countries, the rationale has been about inflation moving to target rather than reacting to weaker growth. This outcome has further boosted sentiment towards risky assets, with equities and corporate bonds performing well.

Against this improving inflation picture, economic growth is holding up and even accelerating in Europe. The rate cuts we see in Europe are evidence of how the central bank’s priority has been, and still is, very much on getting inflation moving to target before easing policy. In Asia, Chinese growth remains lackluster as it continues to cope with the unwinding of property markets, which has affected the region more broadly. Overall, the global economy is enjoying a ‘goldilocks’ scenario of falling inflation and steady growth.

‘The last mile is always the hardest’ is a commonly used phrase when bringing inflation back to target, and this year’s inflation volatility is testimony to that. It means that central banks will be cautious in their rate cuts and likely more reactionary to actual data rather than reducing on the expectation of lower inflation. Furthermore, labour markets in most countries remain robust, with relatively strong wage inflation. Unless there is a surprise slowdown in growth, there is no need for central banks to rush into rate cuts. This backdrop has led to markets performing very well with easy financial conditions. Tighter financial conditions can indeed cause weaker growth, but economies have adapted well to rising rates and prospered.

Risks remain, most obviously, that central banks' caution and looking in the rear-view mirror mean they cut interest rates too slowly, and growth slows more than expected, potentially even into recession. Another risk is that policy is loosened too soon because there are new drivers of inflation that central banks miss. This facilitates growth or inflation surprising to the upside, leading to interest rate hikes restarting.

In summary, we believe that inflation will continue to moderate, dropping back towards central bank targets in the short-to medium-term, with a risk that inflation remains higher for longer because of strong labour markets and wage inflation. So yes, central banks will cut interest rates, but they are in no hurry to do so.

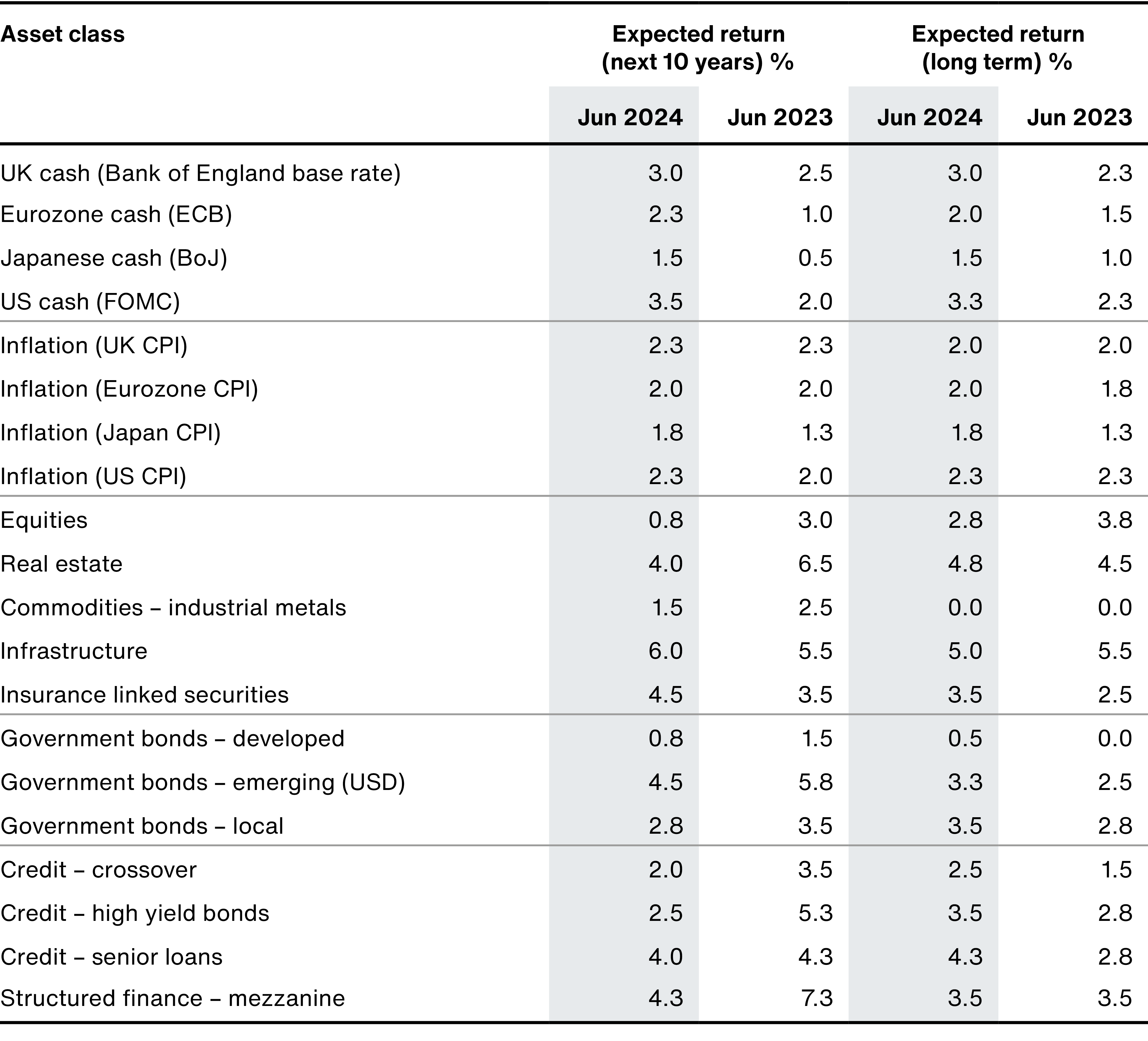

In the following table, we outline our expectations for interest rates and inflation over the next 10 years and beyond, taking account of real growth rates and expected boosts from productivity. Our expectations for asset class returns are above the cash rate on a passive basis, therefore we believe we can add to these figures with active stock selection.

In this summary table and at the end of the asset class outcomes section, we have rounded our forecasts to the nearest 0.25 per cent. This permits a sufficient distinction between asset class returns while avoiding spurious accuracy in our forecasting. Consequently, there may be instances in which numbers quoted in the text do not add up to the stated forecast.

Growth

Following the productivity boost from our recent research into Artificial Intelligence (AI) and industrial policy, as well as the upgrades from our last meeting, we have kept our growth forecasts for most economies unchanged. Our forecasts for average inflation-adjusted growth for the US are 2.2 per cent, for the Eurozone and Japan 1.4 and 1.3 per cent respectively, and for the UK 1.8 per cent over the next 10 years. Across this group, we expect the labour force to stagnate due to an ageing population and lower immigration, so the increase in growth should come from productivity. This is higher than seen in the last decade, though still below the levels experienced during the productivity surge of the 1990s.

For further insights into productivity growth, we have published two papers on our website: The productivity surge of the 2020s and Productivity growth: unravelling the slowdown and forecasting a pick-up.

For emerging markets, excluding China, we forecast real growth of 3.5 per cent, also boosted by AI and industrial policy.

We expect China’s economy to slow over the next decade but still register a respectable 3.4 per cent real growth rate. The shift will follow its transition from an investment-led economic model to one oriented toward domestic consumption.

Inflation

As noted, we expect inflation to converge towards central bank targets over the next decade. The reasons for this include:

- Central banks remain determined to return inflation to their respective targets; their interest rate increases are aimed at curbing demand.

- Supply shortages have eased. Some industries that saw constrained capacity, such as semiconductors and shipping, may well move into oversupply in the medium term, provided there is no exogenous geopolitical shock.

- The Bank of Japan remains comfortable with highly supportive monetary and fiscal policies, further supporting higher inflation expectations, which are currently still below target.

Central banks continue to avoid explicitly referencing average inflation targeting (AIT), which waits for long-term averages to deviate from target before adjusting interest rates. Following the Covid inflation spike, this would have required a period of below-target inflation. There has not been any change in this expectation since our last meeting and so our inflation expectations are unchanged.

In the US, we expect annual consumer price inflation (CPI) to fall only briefly from its current 3.0 per cent rate to below its longer-term target of 2.0 per cent before returning to target for the rest of the decade. That produces an average 10-year inflation figure of 2.2 per cent.

Using the same approach gives us expected inflation of:

- 2.2 per cent in the UK

- 1.9 per cent in the Eurozone

- 1.8 per cent in Japan

- 1.8 per cent in China

- 3.8 per cent in emerging markets outside China

We recognise that this scenario may be wrong, and we remain vigilant regarding some forces that might give rise to higher inflation. These include:

- a shift in political and central bank attitudes, which could lead to inflation targets being de-prioritised or raised,

- more fiscal spending, such as increased defence and infrastructure spending,

- demographic change, where labour participation rates fall, tightening labour markets and raising wage inflation.

Policy rates

We believe policy rates are currently at their peak in all major markets except Japan for this economic cycle. We expect they will begin to fall as inflationary pressure eases because central banks do not want to tighten policy further by allowing the ‘real rate’ – the difference between interest rates and inflation – to rise further. This path should facilitate lower bond yields of longer maturities, which means they would increase in price, albeit the scale of interest rate cuts matters. In thinking about their future trajectory, we place significant weight on factors such as the high levels of global savings, which will also support bonds.

We expect the significant rise in policy rates we have just witnessed to be a relatively short-term phenomenon. That said, we have increased our assumption for the long-term neutral rate in several countries. We think the US policy rate has peaked at 5.4 per cent but will settle at 3.3 per cent vs the 2.9 per cent we expected previously. This reflects the resilience of the US economy to the current level of interest rates while also reflecting risks emanating from domestic politics, geopolitics, government debt levels, and uncertainty over inflation.

Similarly, in the Eurozone and UK, we expect cash rates to fall from their current levels to finish the decade at 2 per cent and 3 per cent respectively, an increase from our last meeting of 0.1 per cent and 0.3 per cent, respectively.

Asset class outcomes

Following a rise in yields, developed market bond returns are slightly more attractive versus cash, and we maintain a small allocation to longer-dated bonds in Australia and the US. We still assign a reasonable probability to a sharper growth slowdown, in which these assets would perform very strongly.

We are still positive about emerging market local currency government bonds, where we forecast a 10-year return of 2.75 per cent above cash. Central banks in the emerging world responded to the rise in inflation by raising interest rates sharply and more quickly than developed market central banks, and they are now starting what we expect to be significant easing cycles over the coming years as inflation subsides.

Similarly, we think hard currency emerging market bonds (those priced in major currencies such as US dollars or euros) can perform well from elevated spreads (which is the amount of yield paid above that of US government debt), which we believe overstate long-run credit risk. We forecast a return of 4.5 per cent above cash.

Returns in mainstream credit markets (investment grade and high yield) are similar to our last iteration. However, following considerable spread tightening (yields have reduced relative to government debt), our return expectations have fallen sharply. Still, spreads above risk-free rates in the structured finance market reflect more default risk than will materialise. We expect this asset class to continue to deliver good long-term returns. For mezzanine bonds, we project a return over cash of 4.25 per cent per annum over the next 10 years.

Recent increases in equity markets and a rise in our expectations for policy rates have made them less attractive. We forecast that returns over the next decade from a global, passive portfolio of 0.75 per cent above cash will still be lower than the long-run expected outcome of 2.75 per cent.

This is partly because corporate profit margins have moved to historically high levels, especially in the US. To be clear, we do not expect a sharp reversal of historical averages. Indeed, we think many companies in the US and elsewhere are capable of sustaining high margins for many years. However, we believe it will be difficult for the whole market to continue generating this profitability level over the very long term. Our forecast, therefore, anticipates a modest degree of future margin compression.

In property, our expected returns are higher than equities at 4 per cent over cash. We expect good outcomes from logistics property in particular. The sector should benefit from growth in ecommerce and the need for adequate warehouse supply in many regions.

In infrastructure, we think the transition from fossil fuel-based generation to new forms of energy provides a significant growth opportunity for both regulated utilities and renewable energy developers and operators. This underpins our 10-year forecast of 6 per cent returns over cash for core infrastructure.

You can find more Multi Asset related content on the insights section of our website. Please contact us if you have any questions regarding this article or any other query related to the strategy.

Risk Factors

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in August 2024 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Potential for profit and loss

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk. Past performance is not a guide to future returns.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.

Important information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

Baillie Gifford Overseas Limited provides investment management and advisory services to non-UK Professional/Institutional clients only. Baillie Gifford Overseas Limited is wholly owned by Baillie Gifford & Co. Baillie Gifford & Co and Baillie Gifford Overseas Limited are authorised and regulated by the FCA in the UK.

Persons resident or domiciled outside the UK should consult with their professional advisers as to whether they require any governmental or other consents in order to enable them to invest, and with their tax advisers for advice relevant to their own particular circumstances.

Financial intermediaries

This communication is suitable for use of financial intermediaries. Financial intermediaries are solely responsible for any further distribution and Baillie Gifford takes no responsibility for the reliance on this document by any other person who did not receive this document directly from Baillie Gifford.

Europe

Baillie Gifford Investment Management (Europe) Ltd (BGE) is authorised by the Central Bank of Ireland as an AIFM under the AIFM Regulations and as a UCITS management company under the UCITS Regulation. BGE also has regulatory permissions to perform Individual Portfolio Management activities. BGE provides investment management and advisory services to European (excluding UK) segregated clients. BGE has been appointed as UCITS management company to the following UCITS umbrella company; Baillie Gifford Worldwide Funds plc. BGE is a wholly owned subsidiary of Baillie Gifford Overseas Limited, which is wholly owned by Baillie Gifford & Co. Baillie Gifford Overseas Limited and Baillie Gifford & Co are authorised and regulated in the UK by the Financial Conduct Authority.

Hong Kong

Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 is wholly owned by Baillie Gifford Overseas Limited and holds a Type 1 license from the Securities & Futures Commission of Hong Kong to market and distribute Baillie Gifford’s range of collective investment schemes to professional investors in Hong Kong. Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 can be contacted at Suites 2713–2715, Two International Finance Centre, 8 Finance Street, Central, Hong Kong. Telephone +852 3756 5700.

South Korea

Baillie Gifford Overseas Limited is licensed with the Financial Services Commission in South Korea as a cross border Discretionary Investment Manager and Non-discretionary Investment Adviser.

Japan

Mitsubishi UFJ Baillie Gifford Asset Management Limited (‘MUBGAM’) is a joint venture company between Mitsubishi UFJ Trust & Banking Corporation and Baillie Gifford Overseas Limited. MUBGAM is authorised and regulated by the Financial Conduct Authority.

Australia

Baillie Gifford Overseas Limited (ARBN 118 567 178) is registered as a foreign company under the Corporations Act 2001 (Cth) and holds Foreign Australian Financial Services Licence No 528911. This material is provided to you on the basis that you are a “wholesale client” within the meaning of section 761G of the Corporations Act 2001 (Cth) (“Corporations Act”). Please advise Baillie Gifford Overseas Limited immediately if you are not a wholesale client. In no circumstances may this material be made available to a “retail client” within the meaning of section 761G of the Corporations Act.

This material contains general information only. It does not take into account any person’s objectives, financial situation or needs.

South Africa

Baillie Gifford Overseas Limited is registered as a Foreign Financial Services Provider with the Financial Sector Conduct Authority in South Africa.

North America

Baillie Gifford International LLC is wholly owned by Baillie Gifford Overseas Limited; it was formed in Delaware in 2005 and is registered with the SEC. It is the legal entity through which Baillie Gifford Overseas Limited provides client service and marketing functions in North America. Baillie Gifford Overseas Limited is registered with the SEC in the United States of America.

The Manager is not resident in Canada, its head office and principal place of business is in Edinburgh, Scotland. Baillie Gifford Overseas Limited is regulated in Canada as a portfolio manager and exempt market dealer with the Ontario Securities Commission (‘OSC’). Its portfolio manager licence is currently passported into Alberta, Quebec, Saskatchewan, Manitoba and Newfoundland & Labrador whereas the exempt market dealer licence is passported across all Canadian provinces and territories. Baillie Gifford International LLC is regulated by the OSC as an exempt market and its licence is passported across all Canadian provinces and territories. Baillie Gifford Investment Management (Europe) Limited (‘BGE’) relies on the International Investment Fund Manager Exemption in the provinces of Ontario and Quebec.

Israel

Baillie Gifford Overseas Limited is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755–1995 (the Advice Law) and does not carry insurance pursuant to the Advice Law. This material is only intended for those categories of Israeli residents who are qualified clients listed on the First Addendum to the Advice Law.

115301 10049293